Don't Rent YOUR Future- Own it

🏡 Renting vs. Buying: What’s the Real Cost Over 2 Years?

If you're on the fence about buying a home versus continuing to rent, you're not alone. With rising home prices and changing interest rates, many people wonder: Is it really worth buying right now? Let's break it down.

We’re going to compare what happens financially when you rent a $500,000 home for 2 years versus buying that same home. The numbers may surprise you.

🔴 Renting for 2 Years

Let’s say you’re paying $3,000/month in rent (which is standard in many parts of the Pacific Northwest right now). Over two years, that adds up to:

-

💸 $3,000 × 24 months = $72,000

-

📉 $0 equity — that’s money you’ll never see again.

-

🚫 No tax benefits — your landlord might be cashing in, but you aren’t.

-

📈 Rent increases likely after the first year.

That’s $72,000 paid… with nothing to show for it.

🟢 Buying a $500,000 Home for 2 Years

Let’s run the numbers for buying the same $500,000 home, with a 3% down payment ($15,000) — and remember, down payment assistance could make that number $0.

-

Loan amount: $485,000

-

Interest rate: 6.5%

-

Monthly P&I (principal + interest): ~$3,065

-

All-in monthly costs (incl. taxes, insurance, PMI): ~$3,500

-

Total payments over 2 years: ~$84,000

Yes — it’s slightly more than renting up front. But here’s what you gain:

-

💰 Principal Paid Down in 2 Years: ~$16,500

-

📈 Home Appreciation (4%/yr): ~$40,800

-

✅ Tax Benefits (Mortgage Interest Deduction): ~$4,500–$6,000

That’s a net gain of $60,000+ in equity, appreciation, and tax savings.

💡 Why This Matters

When you rent, you’re paying someone else’s mortgage — and helping them build wealth. When you own, your money works for you.

Even with a higher monthly cost, the return on ownership makes it clear: in just two years, you could gain over $60,000 in value.

And here’s the bonus: as a homeowner, your payments are fixed, your home could increase in value even more than 4% annually, and you’re building something that’s truly yours.

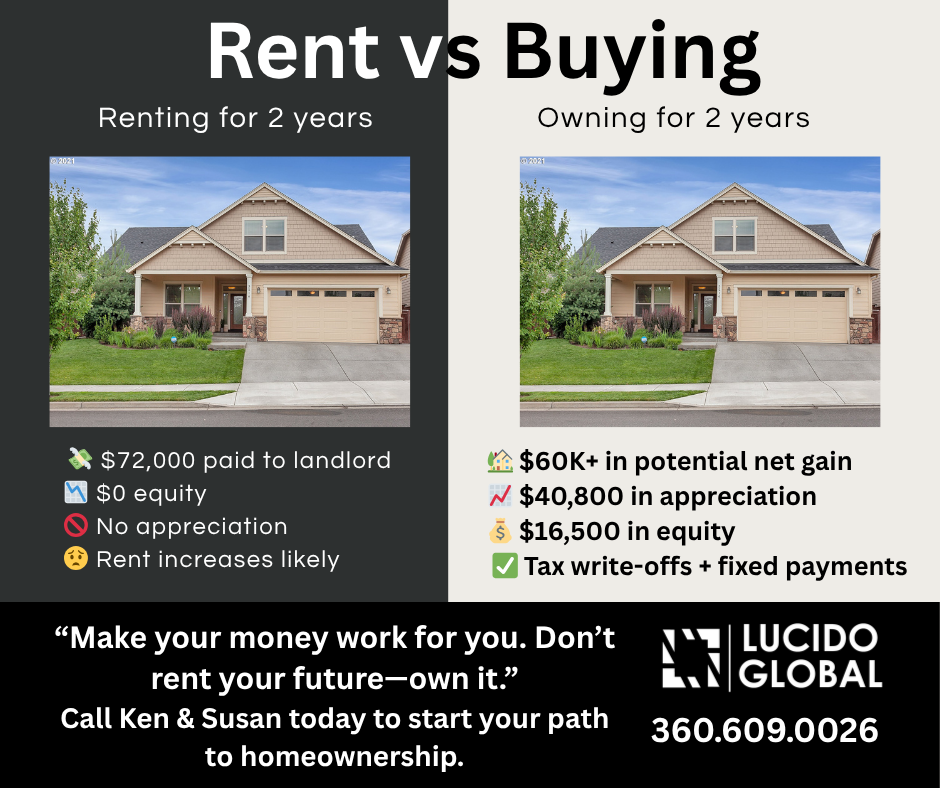

📊 Visual Recap: Renting vs. Buying

Consider this infographic-style breakdown:

➖ Renting (24 Months)

-

💸 $72,000 paid to landlord

-

📉 $0 equity

-

🚫 No appreciation

-

😟 Rent likely to rise

➕ Owning (24 Months)

-

🏡 $60K+ potential net gain

-

📈 $40,800 appreciation

-

💰 $16,500 in equity

-

✅ Tax benefits + stable payments

Ready to Explore Homeownership?

Buying a home isn’t just about shelter — it’s a step toward building wealth. If you're ready to stop renting and start building your future, let’s talk. Whether you're a first-time buyer, need down payment help, or just have questions, we’re here to help you run the numbers and make the right move.

📞 Call Ken & Susan today to get started 360.609.0226

Categories

- All Blogs (612)

- For Sale By Owner (20)

- Local Events (39)

- Portland Metro (1)

- 100 Hands for Foster Care (2)

- 1031 Exchange PNW (1)

- Affordability (58)

- Agent Value (98)

- Battle Ground (1)

- Boutique Neighborhoods (1)

- Brush Prairie WA (1)

- Buying Tips (226)

- Camas WA (1)

- Camas WA Home Buying (1)

- Camas WA Real Estate (1)

- Central Hub (1)

- Clark County Housing (25)

- Closing Costs (1)

- Community Support (17)

- Cowlitz County (1)

- Credit Tips (2)

- Debt-Free Living, (1)

- Design (8)

- Downsize (11)

- Downsizing Vancouver WA (6)

- Economy (28)

- Equity (36)

- Expired Listings (1)

- Featured (20)

- Felida WA Home Buying (1)

- Felida WA Real Estate (1)

- Financial Planning (43)

- First-Time Home Buyer (178)

- For Investors (1)

- For Sale by Owner (6)

- Forecasts (17)

- Foreclosures (6)

- Foster Care Resrources (2)

- Fun Tips (10)

- Giving Back (1)

- Historic Charm (1)

- Historical Character (1)

- Hockinson WA (1)

- Home Buying (297)

- Home Improvement (1)

- Home Inspections (3)

- Home Prep & Staging (5)

- Home Prices (73)

- Home Selling (202)

- Home Staging PNW (1)

- Home Value (10)

- Housing Market Confidence (9)

- Independent Living PNW (2)

- Inventory (38)

- Kalama WA (1)

- La Center (1)

- Landlord Tips (2)

- Lifestyle Move PNW (22)

- Listing Strategy (5)

- Local (61)

- Local Non-Profits (1)

- Longview WA (1)

- Luxury / Vacation (5)

- Market Update (66)

- Mid-Tier Housing (1)

- Mortgage (68)

- Move-Up (13)

- Moving for Job Relocation (1)

- Multi-Generational (1)

- Negotiation Strategy (4)

- New Construction (13)

- Newsletter (13)

- Open House (1)

- Portland Downsizing (4)

- Portland For Sale by Owner (1)

- Portland OR (8)

- Portland OR Affordability (22)

- Portland OR Home Buying (58)

- Portland OR Homes (9)

- Portland OR Real Estate (81)

- Portland OR Seller Tips (20)

- Portland Real Estate FAQs (10)

- Portland Recession Risk (1)

- Portland-Vancouver Home Value (13)

- Portland-Vancouver Inventory (10)

- Price It Right Portland (7)

- Real Estate Investing (8)

- Real Estate Tax Strategy (1)

- Rent vs Buy (18)

- Restaurant Reviews (5)

- Retirement Planning (2)

- Ridgefield WA (1)

- Ridgefield WA Home Buying (1)

- Rightsizing Vancouver WA (3)

- Seasonal (11)

- Selling Rental Property (2)

- selling tips (133)

- Senior Market (5)

- Silver Group (3)

- Suburban Living (3)

- Technology (1)

- Teens & Young Adults (11)

- Trends (15)

- Vancouver For Sale by Owner (1)

- Vancouver WA (9)

- Vancouver WA Affordability (17)

- Vancouver WA Home Buying (45)

- Vancouver WA Home Value (5)

- Vancouver WA Real Estate (82)

- Vancouver WA Selling Tips (20)

- Washougal WA (1)

- Wealth Building (19)

- Yacolt WA (1)

Recent Posts