How to Choose the Right Mortgage for Your Budget

How to Choose the Right Mortgage for Your Budget

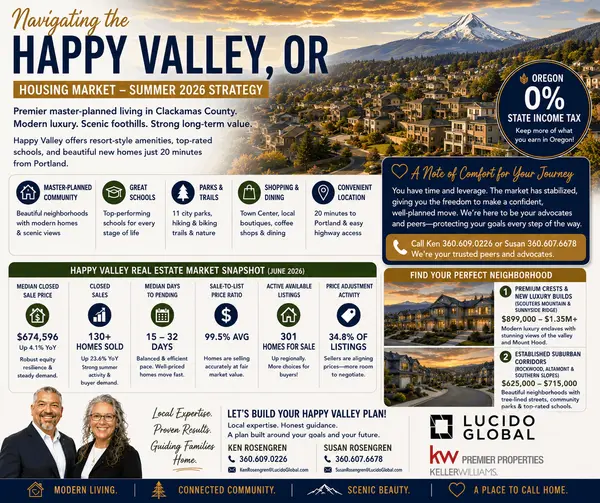

Choosing the right mortgage is one of the most important decisions you’ll make during the homebuying process. With so many options available, it’s essential to understand the different types of loans and which one best fits your financial goals. Here’s a guide to help you choose the right mortgage, along with 9 tips to ensure you’re making a smart decision. We recomend a few proplre for this: Jevon Domench 360.921.6686, Joel Coonrod 360.619.2599 and Alexandrea Key480.487.7071,

1. Understand the Types of Mortgages Available

Before choosing a mortgage, it’s important to understand the different types of loans available. The most common options are fixed-rate mortgages, adjustable-rate mortgages (ARMs), FHA loans, VA loans, and jumbo loans.

Tip 1: Research Government-Backed Loans

If you're a first-time homebuyer or meet specific criteria, consider FHA, VA, or USDA loans. These loans often have lower down payments and more flexible requirements, making homeownership more accessible.

2. Determine How Long You Plan to Stay in the Home

The type of mortgage you choose can be influenced by how long you plan to live in thehome. If you expect to stay in the home for many years, a fixed-rate mortgage may offer stability. If you plan to sell in a few years, an adjustable-rate mortgage (ARM) could save you money.

Tip 2: Consider Short-Term Savings with ARMs

ARMs typically offer lower interest rates for the first few years before adjusting. If you plan to move or refinance before the rate changes, you could benefit from lower initial payments.

3. Compare Interest Rates

Interest rates play a huge role in determining your monthly mortgage payment. Even a small difference in rates can save—or cost—you thousands of dollars over the life of your loan.

Tip 3: Shop Around for the Best Rate

Different lenders offer different rates, so it’s important to shop around and compare offers from multiple mortgage lenders. A lower interest rate can significantly reduce your monthly payment and total interest paid over time.

4. Choose the Right Loan Term

Mortgages typically come in 15-year or 30-year terms. A 30-year mortgage offers lower monthly payments, while a 15-year mortgage allows you to pay off your home faster and save on interest.

Tip 4: Weigh Monthly Payments vs. Long-Term Savings

If you can afford higher monthly payments, a shorter-term mortgage (like 15 years) will save you money on interest in the long run. However, a 30-year loan can provide more flexibility with lower monthly payments.

5. Calculate Your Down Payment

Your down payment is one of the largest upfront costs when buying a home, and it also impacts your loan options. A higher down payment can help you secure better terms or avoid paying private mortgage insurance (PMI).

Tip 5: Aim for a 20% Down Payment

While it’s not required, putting down 20% or more can help you avoid PMI, which can add hundreds of dollars to your monthly payment. It also gives you more equity in your home from the start.

6. Factor in Closing Costs

Closing costs include fees for the appraisal, title insurance, and more, typically totaling 2% to 5% of the loan amount. You’ll need to budget for these expenses on top of your down payment.

Tip 6: Ask the Seller to Cover Some Closing Costs

In some cases, you can negotiate with the seller to cover part of your closing costs. This is especially common in buyer’s markets, where sellers may offer incentives to attract buyers.

7. Look at Your Total Debt-to-Income Ratio

Lenders look closely at your debt-to-income ratio (DTI) to determine if you can afford a mortgage. Your DTI compares your monthly debt payments (including the mortgage) to your monthly income.

Tip 7: Keep Your DTI Below 36%

To qualify for a mortgage, most lenders prefer a DTI ratio of 36% or lower. If your ratio is higher, consider paying down some debts before applying for a mortgage to improve your chances of approval and get better terms.

8. Consider Mortgage Insurance Costs

If you put down less than 20%, most lenders require private mortgage insurance (PMI) on conventional loans. This insurance protects the lender if you default on your loan, but it increases your monthly payment.

Tip 8: Explore Loans with No PMI

Some loan programs, like VA loans for veterans and active-duty service members, don’t require PMI even with lower down payments. Compare your options to see if you qualify for a no-PMI loan.

9. Get Pre-Approved for a Mortgage

Before you start house hunting, it’s a good idea to get pre-approved for a mortgage. A pre-approval letter shows sellers that you’re serious and ready to buy, and it also gives you a clear understanding of how much you can afford.

Tip 9: Choose a Lender That Offers Rate Locks

Once pre-approved, many lenders offer the option to lock in your interest rate for a certain period. This can protect you from rising rates while you search for a home, giving you peace of mind as you move through the process.

Choosing the right mortgage involves careful planning and consideration of your long-term financial goals. By following these steps and tips, you’ll be better equipped to make an informed decision that fits your budget and lifestyle. Remember to take your time, compare offers, and consult with a trusted lender or real estate agent for personalized advice.

Categories

- All Blogs (608)

- For Sale By Owner (20)

- Local Events (39)

- Portland Metro (1)

- 100 Hands for Foster Care (2)

- 1031 Exchange PNW (1)

- Affordability (58)

- Agent Value (98)

- Battle Ground (1)

- Boutique Neighborhoods (1)

- Brush Prairie WA (1)

- Buying Tips (226)

- Camas WA (1)

- Camas WA Home Buying (1)

- Camas WA Real Estate (1)

- Clark County Housing (25)

- Closing Costs (1)

- Community Support (17)

- Cowlitz County (1)

- Credit Tips (2)

- Debt-Free Living, (1)

- Design (8)

- Downsize (11)

- Downsizing Vancouver WA (6)

- Economy (27)

- Equity (35)

- Expired Listings (1)

- Featured (20)

- Felida WA Home Buying (1)

- Felida WA Real Estate (1)

- Financial Planning (43)

- First-Time Home Buyer (178)

- For Investors (1)

- For Sale by Owner (6)

- Forecasts (17)

- Foreclosures (6)

- Foster Care Resrources (2)

- Fun Tips (10)

- Giving Back (1)

- Historic Charm (1)

- Historical Character (1)

- Hockinson WA (1)

- Home Buying (295)

- Home Improvement (1)

- Home Inspections (3)

- Home Prep & Staging (5)

- Home Prices (73)

- Home Selling (200)

- Home Staging PNW (1)

- Home Value (10)

- Housing Market Confidence (7)

- Independent Living PNW (2)

- Inventory (38)

- Kalama WA (1)

- La Center (1)

- Landlord Tips (2)

- Lifestyle Move PNW (22)

- Listing Strategy (5)

- Local (57)

- Local Non-Profits (1)

- Longview WA (1)

- Luxury / Vacation (5)

- Market Update (66)

- Mid-Tier Housing (1)

- Mortgage (68)

- Move-Up (13)

- Moving for Job Relocation (1)

- Multi-Generational (1)

- Negotiation Strategy (4)

- New Construction (13)

- Newsletter (13)

- Open House (1)

- Portland Downsizing (4)

- Portland For Sale by Owner (1)

- Portland OR (8)

- Portland OR Affordability (22)

- Portland OR Home Buying (57)

- Portland OR Homes (9)

- Portland OR Real Estate (77)

- Portland OR Seller Tips (20)

- Portland Real Estate FAQs (10)

- Portland Recession Risk (1)

- Portland-Vancouver Home Value (13)

- Portland-Vancouver Inventory (10)

- Price It Right Portland (7)

- Real Estate Investing (8)

- Real Estate Tax Strategy (1)

- Rent vs Buy (18)

- Restaurant Reviews (5)

- Retirement Planning (2)

- Ridgefield WA (1)

- Ridgefield WA Home Buying (1)

- Rightsizing Vancouver WA (3)

- Seasonal (11)

- Selling Rental Property (2)

- selling tips (133)

- Senior Market (5)

- Silver Group (3)

- Suburban Living (2)

- Technology (1)

- Teens & Young Adults (11)

- Trends (15)

- Vancouver For Sale by Owner (1)

- Vancouver WA (9)

- Vancouver WA Affordability (17)

- Vancouver WA Home Buying (45)

- Vancouver WA Home Value (5)

- Vancouver WA Real Estate (79)

- Vancouver WA Selling Tips (20)

- Washougal WA (1)

- Wealth Building (18)

- Yacolt WA (1)

Recent Posts