What Credit Score Do I Really Need to Buy a Home in Portland or Vancouver?

What Credit Score Do I Really Need to Buy a Home in Portland or Vancouver?

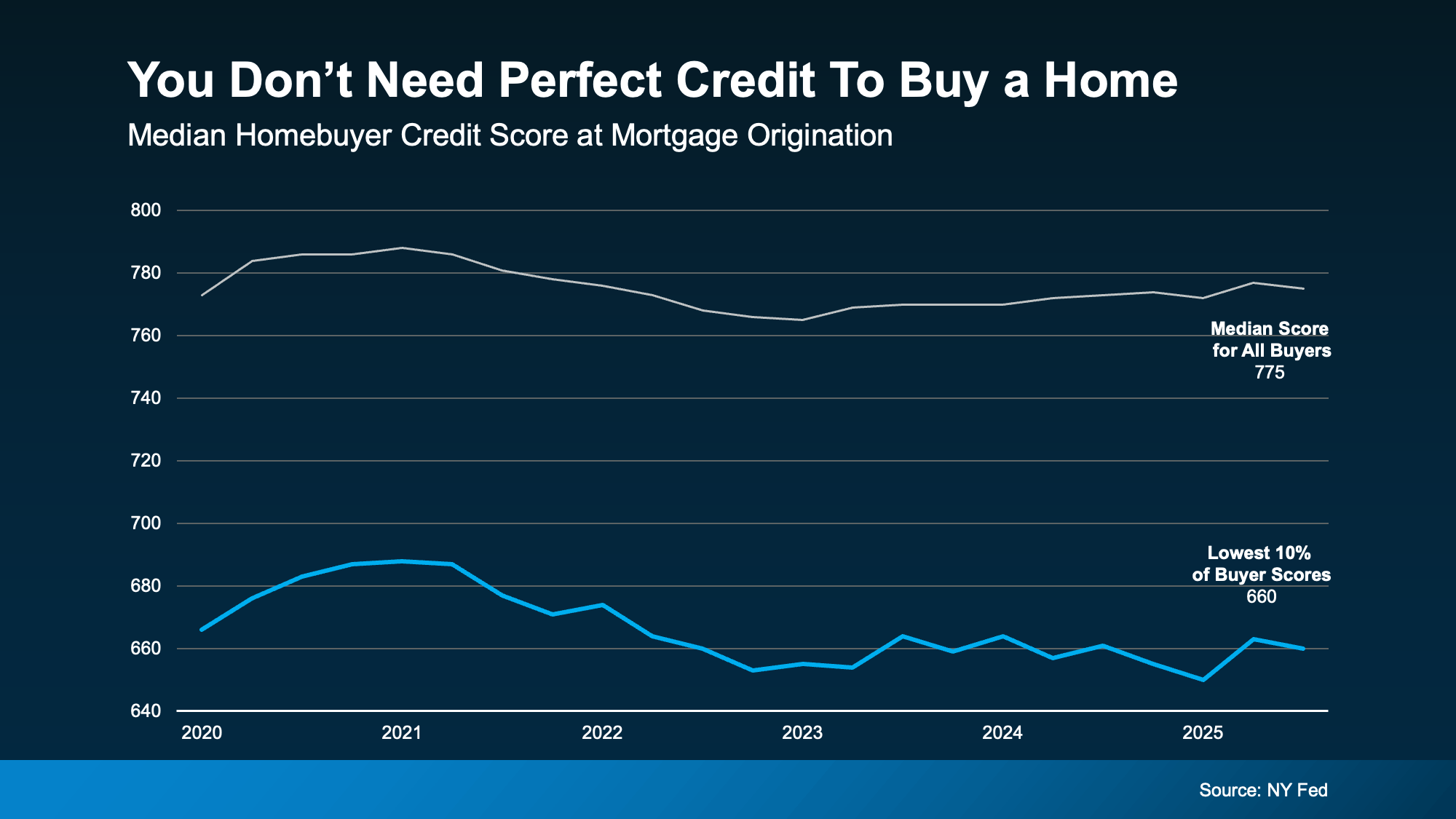

Key Takeaway: You do not need perfect credit to buy a home in 2026. While the median score for PNW buyers is roughly 772, local lenders in Oregon and Washington frequently approve FHA loans with scores as low as 580 (with 3.5% down) or even 500 (with 10% down). In 2026, many local programs now even consider rental and utility payment history to help first-time buyers qualify.

Next Step for You: Since your score determines your interest rate, would you like me to send you a "2026 Credit Quick-Fix" guide? It includes the top 3 ways our clients have boosted their scores by 20+ points in just one billing cycle!

What is the minimum credit score for a mortgage in 2026?

The "minimum" score isn't a single number; it depends entirely on the loan program you choose. In the Portland-Vancouver metro, where the average home price hovers around $545,000, knowing which "bucket" you fall into can save you years of waiting.

2026 Minimum Requirements by Loan Type:

| Loan Type | Typical Minimum Score | Down Payment |

| Conventional | 620 | 3% – 5% |

| FHA (Buyer Favorite) | 580 | 3.5% |

| VA (For Veterans) | 580 – 620 | 0% |

| USDA (Rural/Suburban) | 640 | 0% |

Note: While 580 is the floor for many, having a score of 660+ often unlocks significantly better interest rates, potentially saving you $150–$200 on your monthly payment.

Are there special programs for lower credit in Oregon and Washington?

Are there special programs for lower credit in Oregon and Washington?

Yes. Because our region has high housing costs, local agencies have created "Credit-Flexible" pathways for 2026.

-

Oregon Housing (OHCS) FirstHome: This program offers down payment assistance for buyers with scores as low as 620.

-

WSHFC Home Advantage (WA): In Vancouver, this program provides 4% down payment assistance and even has options for applicants with no credit score by using "alternative" credit like on-time rent and phone bills.

-

Portland Housing Bureau (DPAL): For homes within Portland city limits, second mortgage loans of up to $80,000–$100,000 are available for those who meet income limits, often with more flexible credit underwriting.

How can I improve my score before buying in 2026?

If you're close but not quite there, the "Top 20%" strategy involves three simple moves that can jump your score in 60 days:

-

The 30% Rule: Keep your credit card balances below 30% of your limit.

-

The "No-Inquiry" Period: Stop applying for new credit cards or auto loans at least 6 months before your home search.

-

Rental Reporting: Ask your current landlord to report your on-time payments to the credit bureaus. In 2026, this is a major factor in modern mortgage approvals.

Bottom Line: Don't Disqualify Yourself

Your credit score is a snapshot, not a life sentence. Many people sitting on the sidelines in Camas, Ridgefield, or Portland actually qualify for a home today but don't know it. As a team with 20 years of local experience, we can connect you with the right PNW lenders who specialize in "Credit-Flexible" loans.

Want to know your 2026 "Credit Buying Power"?

Let’s connect for a confidential consultation. We’ve helped 1,000+ people find their way home, and we can help you too.

Lucido Global Team Portland / Vancouver

Phone: 360.609.0226

Email: KenRosengren@LucidoGlobal.com

#CreditScoreMyth #PortlandRealEstate #VancouverWA #Top20PercentAgent #LucidoGlobal #HomeBuying2026 #FirstTimeHomeBuyerPNW #CamasWA #VancouverWAHomes #PortlandORRealtor #RealEstateExpert #MarketLeader #CreditRepairTips #PremierAgent

Categories

- All Blogs (602)

- For Sale By Owner (20)

- Local Events (35)

- Portland Metro (1)

- 100 Hands for Foster Care (2)

- 1031 Exchange PNW (1)

- Affordability (58)

- Agent Value (97)

- Battle Ground (1)

- Boutique Neighborhoods (1)

- Brush Prairie WA (1)

- Buying Tips (226)

- Camas WA (1)

- Camas WA Home Buying (1)

- Camas WA Real Estate (1)

- Clark County Housing (24)

- Closing Costs (1)

- Community Support (17)

- Cowlitz County (1)

- Credit Tips (2)

- Debt-Free Living, (1)

- Design (8)

- Downsize (11)

- Downsizing Vancouver WA (6)

- Economy (27)

- Equity (35)

- Expired Listings (1)

- Featured (20)

- Felida WA Home Buying (1)

- Felida WA Real Estate (1)

- Financial Planning (43)

- First-Time Home Buyer (178)

- For Investors (1)

- For Sale by Owner (6)

- Forecasts (17)

- Foreclosures (6)

- Foster Care Resrources (2)

- Fun Tips (10)

- Giving Back (1)

- Historic Charm (1)

- Historical Character (1)

- Hockinson WA (1)

- Home Buying (295)

- Home Improvement (1)

- Home Inspections (3)

- Home Prep & Staging (5)

- Home Prices (73)

- Home Selling (200)

- Home Staging PNW (1)

- Home Value (10)

- Housing Market Confidence (7)

- Independent Living PNW (2)

- Inventory (38)

- Kalama WA (1)

- La Center (1)

- Landlord Tips (2)

- Lifestyle Move PNW (21)

- Listing Strategy (5)

- Local (52)

- Local Non-Profits (1)

- Longview WA (1)

- Luxury / Vacation (4)

- Market Update (64)

- Mid-Tier Housing (1)

- Mortgage (68)

- Move-Up (12)

- Moving for Job Relocation (1)

- Multi-Generational (1)

- Negotiation Strategy (4)

- New Construction (13)

- Newsletter (13)

- Open House (1)

- Portland Downsizing (4)

- Portland For Sale by Owner (1)

- Portland OR (8)

- Portland OR Affordability (21)

- Portland OR Home Buying (53)

- Portland OR Homes (9)

- Portland OR Real Estate (72)

- Portland OR Seller Tips (20)

- Portland Real Estate FAQs (9)

- Portland Recession Risk (1)

- Portland-Vancouver Home Value (13)

- Portland-Vancouver Inventory (10)

- Price It Right Portland (7)

- Real Estate Investing (8)

- Real Estate Tax Strategy (1)

- Rent vs Buy (18)

- Restaurant Reviews (5)

- Retirement Planning (2)

- Ridgefield WA (1)

- Ridgefield WA Home Buying (1)

- Rightsizing Vancouver WA (3)

- Seasonal (11)

- Selling Rental Property (2)

- selling tips (133)

- Senior Market (5)

- Silver Group (3)

- Suburban Living (2)

- Technology (1)

- Teens & Young Adults (11)

- Trends (15)

- Vancouver For Sale by Owner (1)

- Vancouver WA (8)

- Vancouver WA Affordability (17)

- Vancouver WA Home Buying (45)

- Vancouver WA Home Value (5)

- Vancouver WA Real Estate (78)

- Vancouver WA Selling Tips (20)

- Washougal WA (1)

- Wealth Building (18)

- Yacolt WA (1)

Recent Posts