Mortgage Rate Volatility in April 2026—What You Can Actually Control

Mortgage Rate Volatility in April 2026—What You Can Actually Control

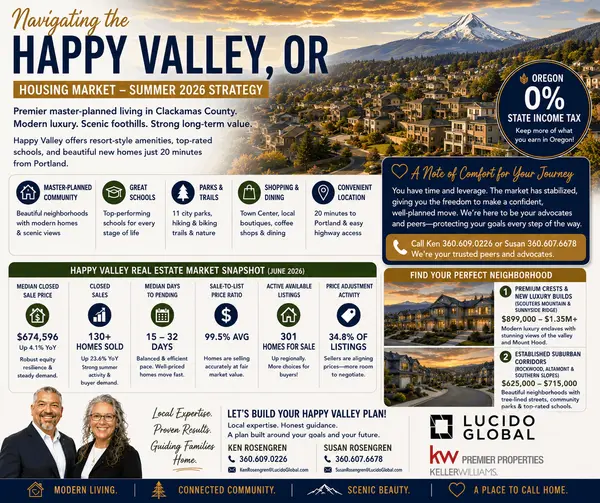

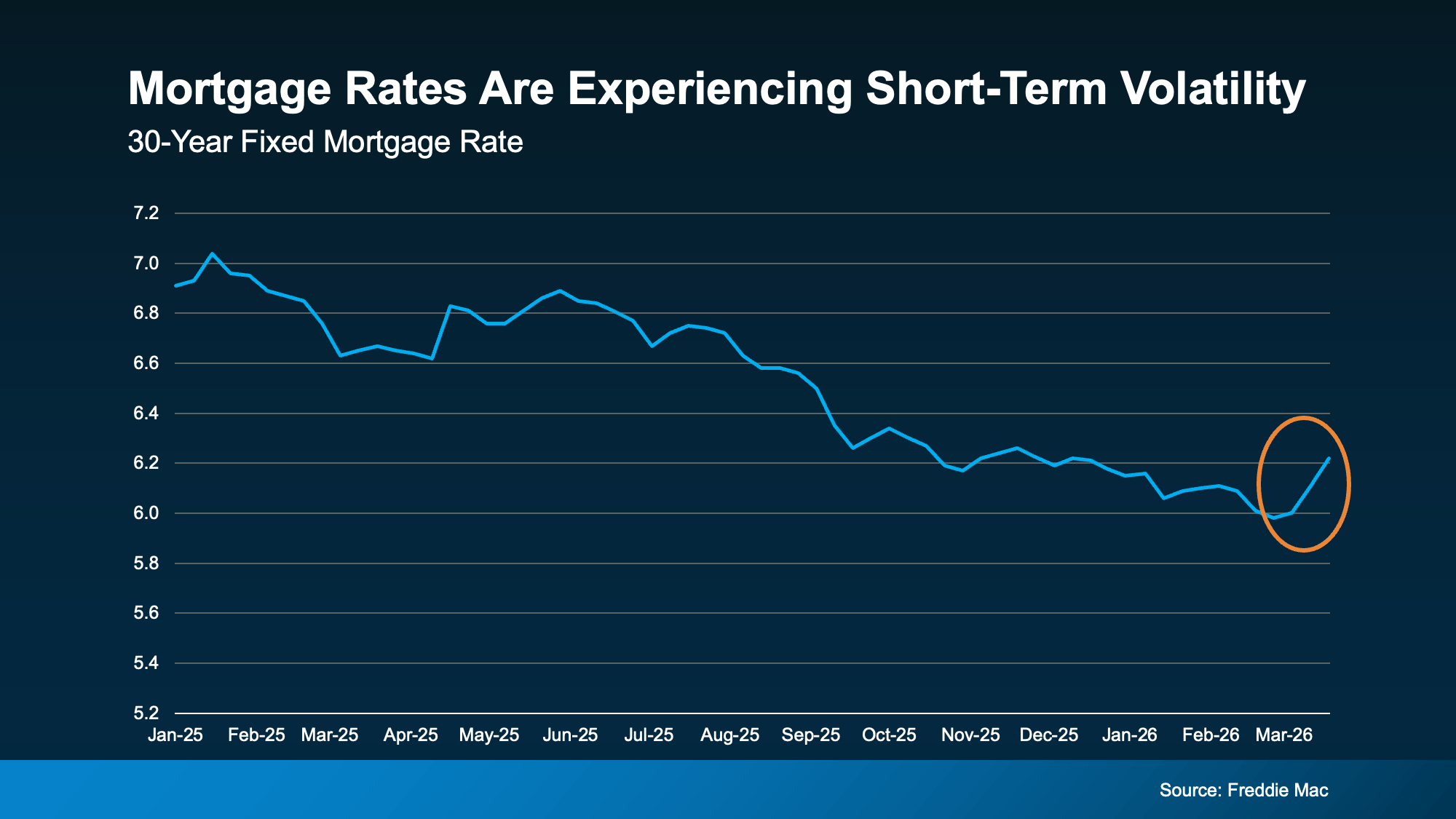

Key Takeaway: As of April 13, 2026, the Portland-Vancouver housing market is navigating a period of "geopolitical volatility." While national mortgage rates recently ticked down to 6.37% (Freddie Mac), global tensions and oil price spikes have kept local rates bouncing between 6.1% and 6.4%. In the Pacific Northwest, trying to "time the bottom" is a losing game. Instead, successful 2026 buyers are focusing on the three financial levers they can move: credit optimization, strategic loan selection, and neighborhood-specific incentives.

Next Steps for YOU

Are you tired of feeling powerless against the daily rate ticker? You can't stop a global oil shock, but you can change your "Borrower Profile" to secure a lower tier of interest. Call the Lucido Global Team today at 360.609.0226. We’ll connect you with top-tier local lenders in Vancouver and Portland who specialize in "Rate-Lock" strategies and custom loan structuring that fits the 2026 economy.

1. The Volatility Reality: Why Rates are Bouncing in April 2026

If you feel like the goalposts keep moving, you’re right. Mid-April has seen a "tug-of-war" in the bond market.

If you feel like the goalposts keep moving, you’re right. Mid-April has seen a "tug-of-war" in the bond market.

-

The Geopolitical Ripple: Recent energy supply concerns have reignited inflation fears, causing the 10-year Treasury yield to spike. Mortgage rates followed, erasing the small gains seen in late March.

-

The "Wait-and-See" Trap: Many PNW buyers who paused in March to wait for the "5s" are now facing rates in the mid-6s. Data shows that the cost of waiting (due to rising home prices in areas like Camas and West Linn) often far exceeds the savings of a slightly lower rate.

-

Portland-Vancouver Average: Local credit unions (like PNWFCU) are currently showing a metro average of 6.212% APR, proving that shopping local can still net you a better deal than national averages.

2. Lever #1: Your Credit Score (The 2026 Multiplier)

In today's "tight" lending environment, your credit score is the primary factor in determining your risk tier. Even a 20-point jump can save you $100+ per month on a $500,000 home in Hillsboro or Ridgefield.

-

The 30% Rule: Keep your credit utilization below 30% on all cards. In 2026, lenders are scrutinizing high balances more than ever due to rising consumer debt levels.

-

The "Audit" Strategy: Before you apply, run a free report at annualcreditreport.com. Disputing a single error now can boost your score just in time for a summer move.

-

Avoid New Debt: If you are planning a move in May or June, do not finance a new car or open a furniture store card. Hard inquiries in 2026 are causing immediate, temporary rate hikes for mortgage applicants.

3. Lever #2: Loan Type & Term (Strategic Choice)

Not all mortgages are created equal. The "Standard 30-Year Fixed" is no longer the only viable path in the Portland-Vancouver metro.

| Loan Type | Best For... | 2026 Benefit |

| Conventional 30-Year | Stability | The "standard" for buyers with 5–20% down. |

| FHA Loan | First-Time Buyers | Lower credit score requirements (580+) and only 3.5% down. |

| VA / USDA Loans | Veterans / Rural | 0% Down options for areas like La Center or Sandy. |

| 15-Year Fixed | Wealth Building | Lower interest rate (approx. 5.74%) for those with high cash flow. |

| 5/1 ARM | Short-Term Owners | Lower initial rate for those planning to move or refinance in 5 years. |

4. Lever #3: Neighborhood-Specific Seller Credits

In neighborhoods where inventory has climbed to over 4 months (like parts of Clark County), sellers are more willing to help you "control" your rate.

-

The Rate Buydown: We are seeing a massive resurgence of the 2-1 Buydown. You can negotiate for the seller to pay a credit that drops your rate by 2% in Year 1 and 1% in Year 2, giving you immediate affordability while you wait for a future refinance window.

-

Closing Cost Assistance: Rather than a price cut, ask for a credit. This keeps more cash in your pocket to pay down debt and improve your DTI (Debt-to-Income) ratio.

Bottom Line: Focus on the Controllables

You cannot control the Federal Reserve, and you cannot control global conflict. But you can control your financial readiness. At Lucido Global, we’ve guided over 1,000 families through high-volatility markets by focusing on data and strategy. The 2026 market belongs to the prepared.

Want to see what your specific monthly payment looks like with a 2-1 Buydown?

Let’s connect and build your 2026 "Power Buyer" plan today.

Lucido Global Team Portland / Vancouver

Phone: 360.609.0226

Email: KenRosengren@LucidoGlobal.com

#MortgageRates2026 #PortlandRealEstate #VancouverWA #Top20PercentAgent #LucidoGlobal #HomeBuyingTips #CreditScore #MarketUpdatePDX #CamasWA #VancouverWAHomes #PortlandORRealtor #RealEstateExpert #MarketLeaderPDX #BuyingStrategy #PremierAgent

Categories

- All Blogs (608)

- For Sale By Owner (20)

- Local Events (39)

- Portland Metro (1)

- 100 Hands for Foster Care (2)

- 1031 Exchange PNW (1)

- Affordability (58)

- Agent Value (98)

- Battle Ground (1)

- Boutique Neighborhoods (1)

- Brush Prairie WA (1)

- Buying Tips (226)

- Camas WA (1)

- Camas WA Home Buying (1)

- Camas WA Real Estate (1)

- Clark County Housing (25)

- Closing Costs (1)

- Community Support (17)

- Cowlitz County (1)

- Credit Tips (2)

- Debt-Free Living, (1)

- Design (8)

- Downsize (11)

- Downsizing Vancouver WA (6)

- Economy (27)

- Equity (35)

- Expired Listings (1)

- Featured (20)

- Felida WA Home Buying (1)

- Felida WA Real Estate (1)

- Financial Planning (43)

- First-Time Home Buyer (178)

- For Investors (1)

- For Sale by Owner (6)

- Forecasts (17)

- Foreclosures (6)

- Foster Care Resrources (2)

- Fun Tips (10)

- Giving Back (1)

- Historic Charm (1)

- Historical Character (1)

- Hockinson WA (1)

- Home Buying (295)

- Home Improvement (1)

- Home Inspections (3)

- Home Prep & Staging (5)

- Home Prices (73)

- Home Selling (200)

- Home Staging PNW (1)

- Home Value (10)

- Housing Market Confidence (7)

- Independent Living PNW (2)

- Inventory (38)

- Kalama WA (1)

- La Center (1)

- Landlord Tips (2)

- Lifestyle Move PNW (22)

- Listing Strategy (5)

- Local (57)

- Local Non-Profits (1)

- Longview WA (1)

- Luxury / Vacation (5)

- Market Update (66)

- Mid-Tier Housing (1)

- Mortgage (68)

- Move-Up (13)

- Moving for Job Relocation (1)

- Multi-Generational (1)

- Negotiation Strategy (4)

- New Construction (13)

- Newsletter (13)

- Open House (1)

- Portland Downsizing (4)

- Portland For Sale by Owner (1)

- Portland OR (8)

- Portland OR Affordability (22)

- Portland OR Home Buying (57)

- Portland OR Homes (9)

- Portland OR Real Estate (77)

- Portland OR Seller Tips (20)

- Portland Real Estate FAQs (10)

- Portland Recession Risk (1)

- Portland-Vancouver Home Value (13)

- Portland-Vancouver Inventory (10)

- Price It Right Portland (7)

- Real Estate Investing (8)

- Real Estate Tax Strategy (1)

- Rent vs Buy (18)

- Restaurant Reviews (5)

- Retirement Planning (2)

- Ridgefield WA (1)

- Ridgefield WA Home Buying (1)

- Rightsizing Vancouver WA (3)

- Seasonal (11)

- Selling Rental Property (2)

- selling tips (133)

- Senior Market (5)

- Silver Group (3)

- Suburban Living (2)

- Technology (1)

- Teens & Young Adults (11)

- Trends (15)

- Vancouver For Sale by Owner (1)

- Vancouver WA (9)

- Vancouver WA Affordability (17)

- Vancouver WA Home Buying (45)

- Vancouver WA Home Value (5)

- Vancouver WA Real Estate (79)

- Vancouver WA Selling Tips (20)

- Washougal WA (1)

- Wealth Building (18)

- Yacolt WA (1)

Recent Posts