Should a Buyer Wait for Interest Rates to Drop from 6.5% to 5.5%?

Categories

- All Blogs (614)

- For Sale By Owner (20)

- Local Events (39)

- Portland Metro (1)

- 100 Hands for Foster Care (2)

- 1031 Exchange PNW (1)

- Affordability (58)

- Agent Value (98)

- Battle Ground (1)

- Boutique Neighborhoods (1)

- Brush Prairie WA (1)

- Buying Tips (226)

- Camas WA (1)

- Camas WA Home Buying (1)

- Camas WA Real Estate (1)

- Central Hub (1)

- Clark County Housing (25)

- Closing Costs (1)

- Community Support (17)

- Cowlitz County (1)

- Credit Tips (2)

- Debt-Free Living, (1)

- Design (8)

- Downsize (11)

- Downsizing Vancouver WA (6)

- Economy (28)

- Equity (36)

- Expired Listings (1)

- Featured (20)

- Felida WA Home Buying (1)

- Felida WA Real Estate (1)

- Financial Planning (43)

- First-Time Home Buyer (178)

- For Investors (1)

- For Sale by Owner (6)

- Forecasts (17)

- Foreclosures (6)

- Foster Care Resrources (2)

- Fun Tips (10)

- Giving Back (1)

- Historic Charm (1)

- Historical Character (1)

- Hockinson WA (1)

- Home Buying (297)

- Home Improvement (1)

- Home Inspections (3)

- Home Prep & Staging (5)

- Home Prices (73)

- Home Selling (203)

- Home Staging PNW (1)

- Home Value (10)

- Housing Market Confidence (10)

- Independent Living PNW (2)

- Inventory (38)

- Kalama WA (1)

- La Center (1)

- Landlord Tips (2)

- Lifestyle Move PNW (22)

- Listing Strategy (5)

- Local (62)

- Local Non-Profits (1)

- Longview WA (1)

- Luxury / Vacation (5)

- Market Update (66)

- Mid-Tier Housing (1)

- Mortgage (68)

- Move-Up (13)

- Moving for Job Relocation (1)

- Multi-Generational (1)

- Negotiation Strategy (4)

- New Construction (14)

- Newsletter (13)

- Open House (1)

- Portland Downsizing (4)

- Portland For Sale by Owner (1)

- Portland OR (8)

- Portland OR Affordability (22)

- Portland OR Home Buying (60)

- Portland OR Homes (9)

- Portland OR Real Estate (83)

- Portland OR Seller Tips (20)

- Portland Real Estate FAQs (10)

- Portland Recession Risk (1)

- Portland-Vancouver Home Value (13)

- Portland-Vancouver Inventory (10)

- Price It Right Portland (7)

- Real Estate Investing (8)

- Real Estate Tax Strategy (1)

- Rent vs Buy (18)

- Restaurant Reviews (5)

- Retirement Planning (2)

- Ridgefield WA (1)

- Ridgefield WA Home Buying (1)

- Rightsizing Vancouver WA (3)

- Seasonal (11)

- Selling Rental Property (2)

- selling tips (133)

- Senior Market (5)

- Silver Group (3)

- Suburban Living (3)

- Technology (1)

- Teens & Young Adults (11)

- Trends (15)

- Vancouver For Sale by Owner (1)

- Vancouver WA (9)

- Vancouver WA Affordability (17)

- Vancouver WA Home Buying (47)

- Vancouver WA Home Value (5)

- Vancouver WA Real Estate (84)

- Vancouver WA Selling Tips (20)

- Washougal WA (1)

- Wealth Building (19)

- Yacolt WA (1)

Recent Posts

Think Nobody's Buying Homes Right Now? Think Again—The Metro Portland & SW Washington Seller Strategy

The "Take It or Leave It" Era Is Over—What Concessions & Incentives Mean for You in Metro Portland & SW Washington

What Buying or Selling a Home Gives Back to the Metro Portland & SW Washington Community

Why the Metro Portland & Vancouver WA Housing Market Is Stronger Than You Think

Navigating the Tigard, OR Housing Market—The Summer 2026 Strategy

The #1 Factor Explaining Metro Portland & Vancouver WA Home Prices Right Now

Navigating the Beaverton, OR Housing Market—The Summer 2026 Strategy

Portland Metro Housing Market Update: June 2026 RMLS Data & Expert Analysis

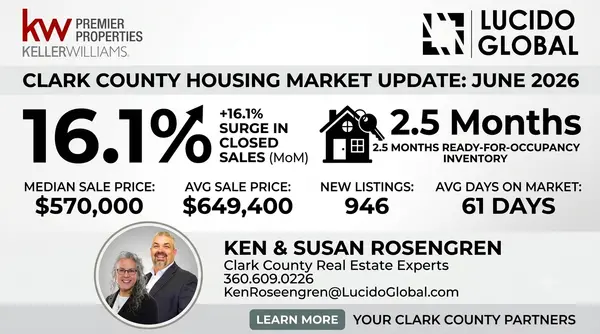

Clark County Housing Market Update: June 2026 RMLS Data & Expert Analysis

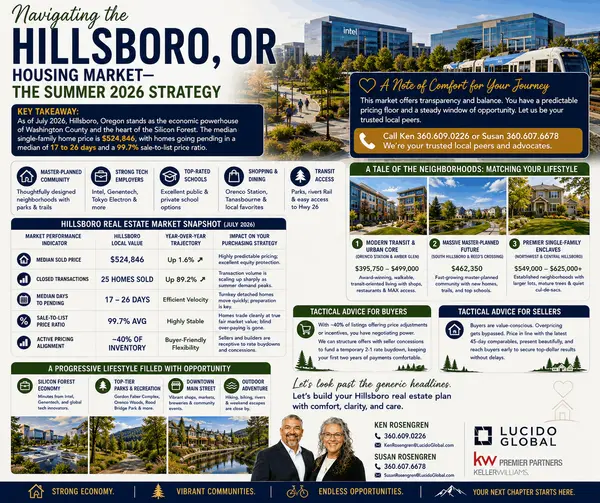

Navigating the Hillsboro, OR Housing Market—The Summer 2026 Strategy