Mortgage Rate Forecast: Why Lower Rates Are Coming to Vancouver WA and Portland OR

You want mortgage rates to fall, and they’ve started to. But is the current trend going to last? And how much relief can buyers in Vancouver WA and Portland OR realistically expect?

Experts say there’s room for rates to come down even more over the next year, and the most reliable indicators—the 10-Year Treasury Yield and the Spread—are pointing toward a more affordable 2026.

The Key Indicators: Yield and Spread Explained

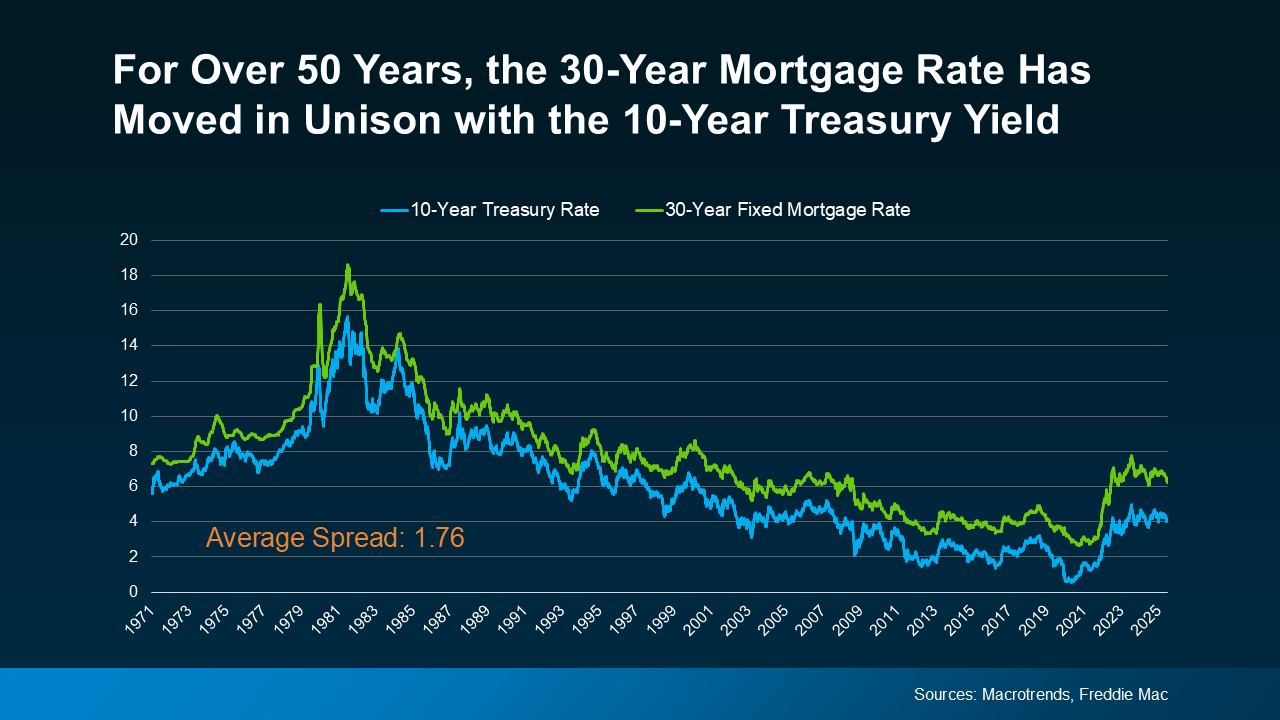

For over 50 years, the 30-year fixed mortgage rate has closely followed the movement of the 10-year Treasury yield, a widely watched benchmark for long-term interest rates.

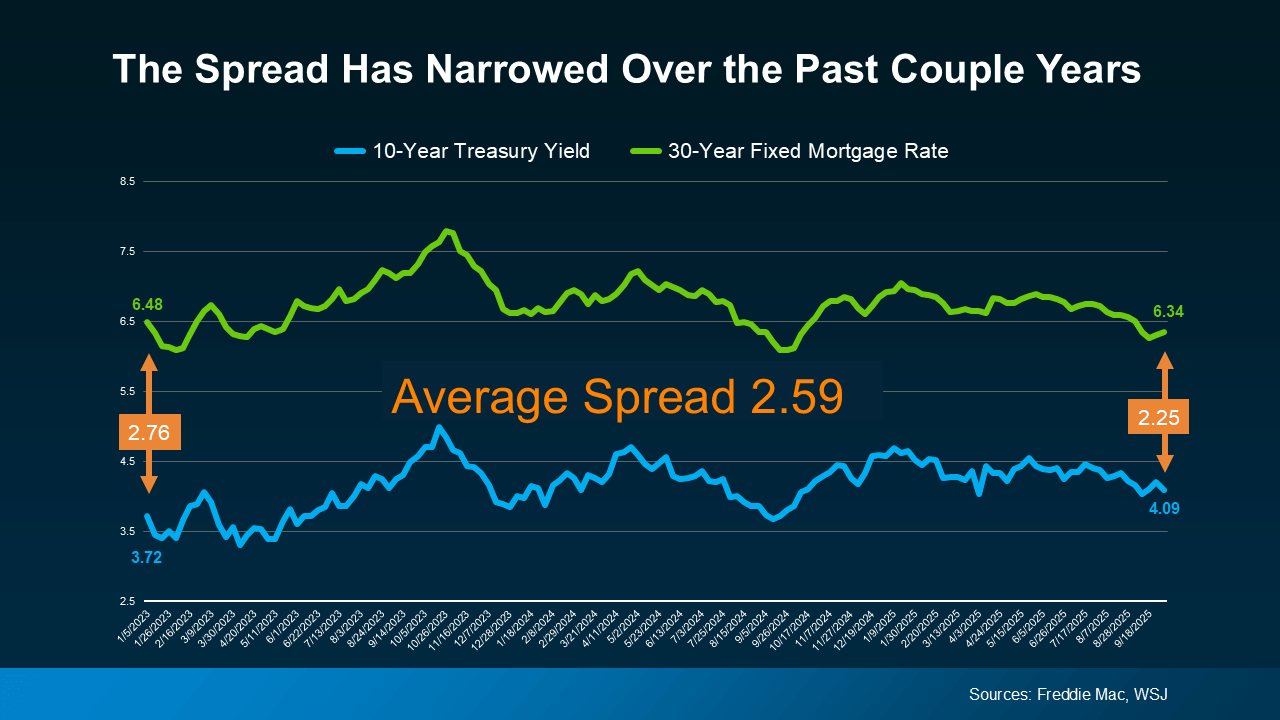

1. The Shrinking Spread is Your Sign of Relief

The Spread is the gap between the 10-year Treasury yield and the 30-year mortgage rate, which typically averages about 1.76 percentage points (176 basis points). Over the past few years, this spread widened well beyond normal due to market uncertainty and fear, pushing mortgage rates artificially high.

-

Why it matters: The wide spread was effectively a "risk premium" baked into your rate. Now, as the economy's path becomes clearer, this spread is starting to shrink. A shrinking spread means a lower mortgage rate, even if the Treasury yield itself remains stable. This is a crucial sign of health for the Portland-Vancouver housing market.

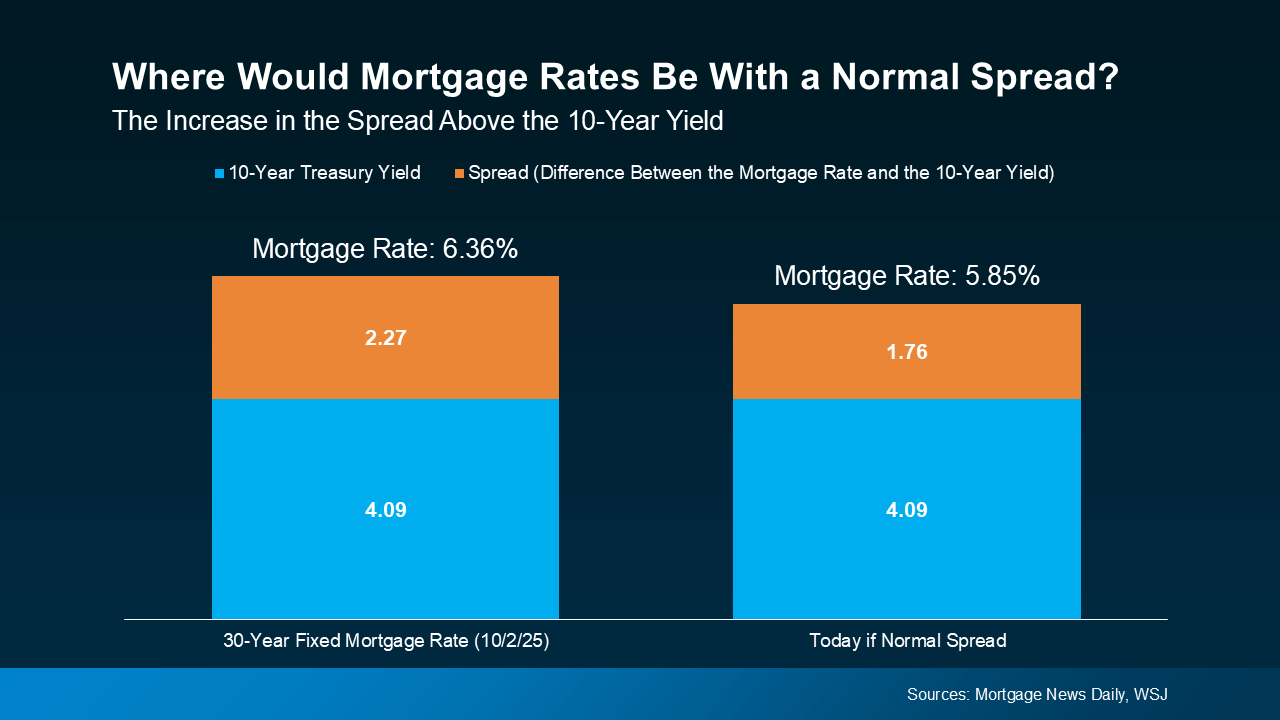

2. The 10-Year Treasury Yield is Expected to Decline

2. The 10-Year Treasury Yield is Expected to Decline

It’s not just the shrinking spread, though. Experts also forecast the 10-year Treasury yield itself to come down in the months ahead as inflation eases.

When you combine a lower yield with a narrowing spread, you have two powerful forces potentially pushing mortgage rates down.

What This Means for Your Monthly Payment in the Pacific Northwest

This long-term economic relationship is the primary reason major housing authorities are now projecting a gradual decline in mortgage rates through 2026.

Current Rate Forecast for the Vancouver/Portland Metro Area:

The potential for rates to dip below 6% by late 2026 is not just an arbitrary number—it’s a psychological and financial tipping point for our local market.

The Financial Impact for Local Buyers

A drop of even half a percentage point can be huge for affordability in the Vancouver WA and Portland OR area where home prices are elevated:

-

Example: On a typical $450,000 loan, dropping the rate from 6.5% to 6.0% can save a buyer over $150 per month on their principal and interest payment alone. This change restores significant buying power that was lost when rates spiked.

The Bigger Risk: Waiting Too Long

While the downward trend is encouraging, industry experts warn that waiting for a specific "magic number" (like 5.9%) could be a costly mistake.

Lower rates will unlock massive pent-up demand. When that happens, the less-competitive, inventory-rich market we have now will quickly give way to intense bidding wars, pushing home prices up sharply in Vancouver and Portland. Paying today's rate and refinancing later could be far less costly than waiting and being forced to compete for a home that costs $25,000 to $50,000 more.

Bottom Line: Plan Your Move Now

Keeping up with the Treasury Yield, the Spread, and the latest forecasts can feel overwhelming. That’s why having an experienced local Vancouver WA and Portland OR real estate team on your side matters. We translate these complex economic dynamics into a clear strategy for your purchase or sale.

Don't wait for the absolute lowest rate to start your search. Let’s connect today to discuss a refinance strategy and help you capitalize on the current market's lower competition before a wave of new buyers joins the race in 2026.

Categories

- All Blogs (608)

- For Sale By Owner (20)

- Local Events (39)

- Portland Metro (1)

- 100 Hands for Foster Care (2)

- 1031 Exchange PNW (1)

- Affordability (58)

- Agent Value (98)

- Battle Ground (1)

- Boutique Neighborhoods (1)

- Brush Prairie WA (1)

- Buying Tips (226)

- Camas WA (1)

- Camas WA Home Buying (1)

- Camas WA Real Estate (1)

- Clark County Housing (25)

- Closing Costs (1)

- Community Support (17)

- Cowlitz County (1)

- Credit Tips (2)

- Debt-Free Living, (1)

- Design (8)

- Downsize (11)

- Downsizing Vancouver WA (6)

- Economy (27)

- Equity (35)

- Expired Listings (1)

- Featured (20)

- Felida WA Home Buying (1)

- Felida WA Real Estate (1)

- Financial Planning (43)

- First-Time Home Buyer (178)

- For Investors (1)

- For Sale by Owner (6)

- Forecasts (17)

- Foreclosures (6)

- Foster Care Resrources (2)

- Fun Tips (10)

- Giving Back (1)

- Historic Charm (1)

- Historical Character (1)

- Hockinson WA (1)

- Home Buying (295)

- Home Improvement (1)

- Home Inspections (3)

- Home Prep & Staging (5)

- Home Prices (73)

- Home Selling (200)

- Home Staging PNW (1)

- Home Value (10)

- Housing Market Confidence (7)

- Independent Living PNW (2)

- Inventory (38)

- Kalama WA (1)

- La Center (1)

- Landlord Tips (2)

- Lifestyle Move PNW (22)

- Listing Strategy (5)

- Local (57)

- Local Non-Profits (1)

- Longview WA (1)

- Luxury / Vacation (5)

- Market Update (66)

- Mid-Tier Housing (1)

- Mortgage (68)

- Move-Up (13)

- Moving for Job Relocation (1)

- Multi-Generational (1)

- Negotiation Strategy (4)

- New Construction (13)

- Newsletter (13)

- Open House (1)

- Portland Downsizing (4)

- Portland For Sale by Owner (1)

- Portland OR (8)

- Portland OR Affordability (22)

- Portland OR Home Buying (57)

- Portland OR Homes (9)

- Portland OR Real Estate (77)

- Portland OR Seller Tips (20)

- Portland Real Estate FAQs (10)

- Portland Recession Risk (1)

- Portland-Vancouver Home Value (13)

- Portland-Vancouver Inventory (10)

- Price It Right Portland (7)

- Real Estate Investing (8)

- Real Estate Tax Strategy (1)

- Rent vs Buy (18)

- Restaurant Reviews (5)

- Retirement Planning (2)

- Ridgefield WA (1)

- Ridgefield WA Home Buying (1)

- Rightsizing Vancouver WA (3)

- Seasonal (11)

- Selling Rental Property (2)

- selling tips (133)

- Senior Market (5)

- Silver Group (3)

- Suburban Living (2)

- Technology (1)

- Teens & Young Adults (11)

- Trends (15)

- Vancouver For Sale by Owner (1)

- Vancouver WA (9)

- Vancouver WA Affordability (17)

- Vancouver WA Home Buying (45)

- Vancouver WA Home Value (5)

- Vancouver WA Real Estate (79)

- Vancouver WA Selling Tips (20)

- Washougal WA (1)

- Wealth Building (18)

- Yacolt WA (1)

Recent Posts